The Race-Based Mortgage PenaltyAlso, the food tastes terrible and the portions are so small!By THE EDITORIAL BOARD MARCH 7, 2018

As the Trump administration begins to gut federal enforcement of civil rights laws, minority communities that were targets for predatory home loans before the recession have become vulnerable yet again to mortgage discrimination. This time, many banks are simply writing off communities of color and denying them loans at all.

An alarming new study by the Center for Investigative Reporting’s online publication Reveal found that African-Americans and Latinos were far more likely to be denied conventional mortgages than whites even when income, loan size and other factors were taken into account.But … “Credit score was not included because that information is not publicly available” according to Reveal.

So, their regression analysis was basically worthless.

The study examined 31 million mortgage records and found disturbing evidence in 61 metropolitan areas … Black applicants were disproportionately turned away, as compared to whites, in 48 metropolitan areas, Latinos in 25, Asian-Americans in nine and Native Americans in three areas. In Washington, D.C., the study found that all four groups were far more likely to be denied home loans than were whites. …I’m confused. Is the problem that lenders racistly loaned too enthusiastically to nonwhites or not enthusiastically enough? Or both?Banks have subverted the purpose of the Community Reinvestment Act of 1977, which was supposed to get them to lend and invest more, and open more branches, in low- and moderate-income areas. This was to correct decades of damage the federal government caused by encouraging lenders to ignore black areas until the passage of the federal Fair Housing Act in 1968. The Reveal study found that affordable mortgages issued in historically black neighborhoods to comply with the reinvestment act were going to white newcomers instead of longtime black residents. This has accelerated a pattern of gentrification that forces out black residents. …

Upper-income black people were even more likely to be denied loans, as compared to similarly situated whites, than lower income black people were to their white counterparts. This underscored yet again that African-Americans cannot escape economic discrimination simply by becoming wealthier, especially when financial institutions persist in punishing them for living in majority minority neighborhoods.

… By denying African-American families mortgage credit, the financial industry also denies them the opportunity to accumulate household wealth — part of the reason that white median family net worth is nearly 10 times that of black families.

Beyond that, the decision to withhold credit from minority neighborhoods has turned too many of them into hollowed-out areas with high poverty, failing schools, lower property values and a markedly worse quality of life.It’s a mystery wrapped inside a riddle inside an enigma.Not long ago, fair housing groups that uncovered particularly egregious lending discrimination by banks and mortgage companies could count on federal regulators to curb, at least, the worst forms of predation. …

Banks often claim that they deny mortgages in minority communities based on credit scores — but that claim is almost impossible to check, given that the credit scores are not publicly available.

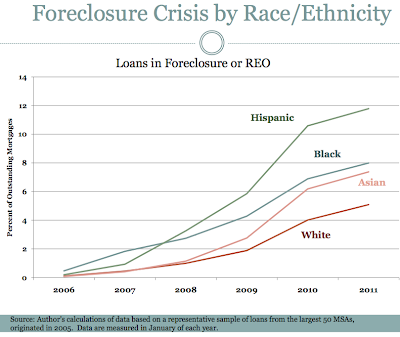

Here’s a graph created by Dr. Caroline Reid of the San Francisco Fed who almost nobody but my readers has ever seen. Default rates by ethnicity among the disastrous 2005 vintage of mortgages:

But who can remember the past when virtually nobody was ever told about the present?

iSteve Commenter Seth Largo adds:

The push to ensconce blacks and Hispanics in single family homes connects nicely with Steve’s running thesis regarding the mass luring of these demographic groups from the urban core to the suburbs and exurbs. If we can start handing out mortgages like candy again, we can get back to those golden days in 2005 when blacks and Hispanics were moving out to Adelanto and Ferguson instead of standing their ground in Boyle Heights.[Comment at Unz.com]